“How romantic this couple is. See the old man is lovingly gifting gold bangles to his wife on their anniversary.” More than this advertisement, my words were enough to shock my husband who was ‘half-heartedly’ sitting and watching my favourite serial with me. I always hate TV commercials, and if they come between my favourite serials, my hatred sees no limits, and I start cursing makers. But somehow this commercial managed to grab my attention. After all, it was a sweet advertisement in which the wife was scolding his retired husband for buying such a costly gift on the anniversary. But even the wife couldn’t stop herself from smiling when her husband proudly said that she deserved it and he had planned enough for retirement.

My husband got a second shock when instead of asking for the same costly gift, I said, “Will we also have the same financially secured life after retirement?” My husband preferred to stay silent in response.

Gene Perret, the famous comedy writer, once written about retirement, “it’s nice to get out of the rat race, but you have to get along with less cheese.” Almost everyone looks forward to that time when they can live a worry-free life, away from the hustle and bustle of office life. On the one hand, retirement gives ample time to enjoy the rest of the life; it also compels you to think: How to finance your needs?

Throughout the life, we work hard to meet requirements of our family. Many things are sidelined to make the life of our family easy, and retirement planning is one of them. Nothing comes easily, and as time passes, things become more difficult with age— both physically and financially. As a result, for most of the salaried professionals, retirement planning revolves around employee provident fund (EPF) only. Well, there is nothing wrong with the provident fund. In fact, the contribution is linked to the salary and increases with an increment. But by itself, PF is not sufficient for retirement because of the following reasons:

- With the inflation rate hovering between 7% and 8%, provident funds alone barely beat the inflation rate. For instance, a 35-year old, whose monthly basic salary is Rs 50,000, contributes Rs 6000/month in his PF account. His employer is also contributing the similar amount to his EPF account. He expects an average annual increase of 10% in his salary and current EPF balance is Rs 10,000. By the time he retires at the age of 60, his provident fund balance will be close to Rs 1.6 crores, assuming the EPF interest rate as 9%. While Rs 1.6 crores may look huge but it may not be enough to secure his retirement life. If his current monthly expenses are 30,000, 8% inflation rate will increase his monthly expenses requirements to roughly Rs 2.05 lakhs/month after 25 years from now. It means, Rs 1.6 crores from PF would be wiped out in a little over six years, and he would be left with no money in his retirement corpus after the age of 66 years.

- The power of compounding works over a longer tenure, and therefore, to build a huge corpus, you need to stay invested for a longer time. However, many people withdraw their provident fund amount when they change their jobs, and thus, losing out a lot of substantial amounts.

- Healthcare is increasingly becoming unaffordable for people owing to high medical treatment costs in the recent years. A single hospitalisation can wipe out your life’s savings. Further, with an increase in age, a person becomes more susceptible to ailments and needs frequent medical treatment. Simple cataract surgery can cost you somewhere between Rs 20,000 and Rs 40,000. Your provident fund amount may not be able to deal with the soaring medical inflation rate.

- The rising cost of living has increased in the country. In the last five years, the prices of essential commodities, such as milk, pulses, and oil have increased by over 70%. Your provident fund amount will not be sufficient to beat the high cost of living which will only grow shortly.

- In India, life expectancy ratio has increased over the years. As per the statistics released by the Union Ministry of Health and Family Welfare, life expectancy ratio has increased by five years, from 62.3 years for males and 63.9 years for females in 2001-05 to 67.3 years and 69.6 years respectively in 2011-15. The longer you live, the more your expenses are; and which means, you need more money to sustain your living. Your provident fund may fail to deal with the rising money requirements.

- Only salaried professionals have the option of contribution in a provident fund. It means, self-employed professionals, such as lawyers, and doctors, have to look out for some other retirement planning options.

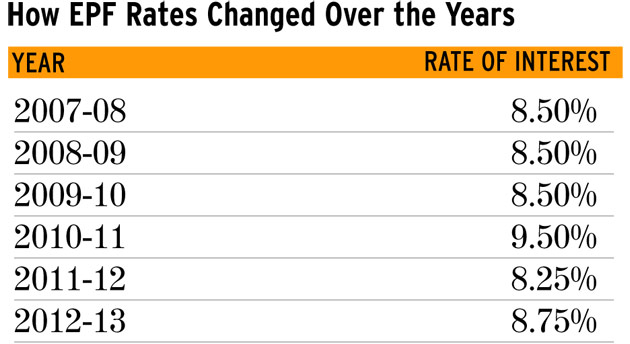

The following graph shows how EPF interest rates have been declining in the past few years. It means net returns from provident funds will not be sufficient to meet your post-retirement needs.

Now, where to invest

The financial market is flooded with various investment products whose makers put all their persuasive powers to make you believe that their plan is the best retirement solution. However, as an investor, you should ensure that you do not carry away by high-pitched marketing tactics and choose an investment product that takes care of your retirement needs.

Here, Unit-Linked Insurance Plans (ULIPs) retirement plans fit well in the picture. These plans build a vast retirement corpus, which can be further channelised to generate regular income through annuity plans. Here are some other benefits of ULIP retirement plans:

- Assured Benefits: Various ULIP retirement plans offer assured benefits to safeguard the lifetime saving of pensioners from the market volatility. These guaranteed maturity benefits have made ULIPs an attractive investment option. Some insurance plans offer an assured benefit or fund value, whichever is higher, at the time of maturity. Here, assured benefit is 101% of the sum of all premiums paid. Also, you can increase your retirement corpus through pension boosters.

- High returns in the long run: A part of the premium is invested in equity funds to generate high returns. As a result, ULIP retirement plans have the potential to generate better returns over the long run as compared to provident funds.

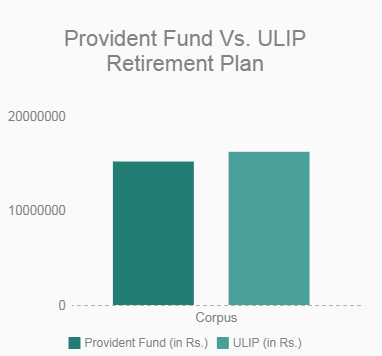

Let’s understand it with an example.

Mr Suresh, a 35-year old IT professional, contributes 12% of his basic salary i.e., Rs 3000, to the provident fund. If he also invests 15% of his annual income, which is Rs 12,00,000, for his retirement in a ULIP retirement plan, he would be able to build a much bigger corpus than what he will get from the provident fund account at the age of 65, as shown below:-

- Great flexibility: ULIPs are flexible products that let you invest as per your risk appetite and age. It means, if there is a long time before your retirement, you can take more risk and invest in equities. Similarly, when you are near to your retirement, you can invest in low-risk debt funds. Further, it is not a one-time You can use fund switching options to alter your fund mix during the policy tenure.

- Transparent structure: ULIP plans have transparent structure, which means, all commissions and charges are explicitly detailed in the policy document. Also, all charges are evenly distributed throughout the policy tenure. It is better than the other investment products which are front-loaded, and the entire first-year premium goes towards in charges.

- Regular pension for life: With ULIP retirement plans, you can get a regular pension for life. In case of your death, your spouse would be entitled to get the pension amount.

- Insurance coverage for the family: In case of sudden demise of the policyholder, the insurer offers death benefits to the nominee.

- Easy to buy: All you need is good internet connection, and you can purchase ULIP retirement plans online from the comfort of your home, working in an office or while travelling. It makes the entire buying process hassle-free.

“Retire from Work, but not from Life”- M.K Soni

Retirement is a happy phase of life when there are no project deadlines to meet, no fear for Mondays and no nasty boss. You can simply set your own work schedule, take long vacations and pursue your hobbies. However, as it is said, “The early bird catches the worm”, the planning for retirement is a long-term process, and earlier you start it, better returns you get. Further, life expectancy has also increased by five years in a decade. Therefore, it becomes essential to plan well if you want to have a financially secured life after retirement.

EPF Image Source: Business Today

6,007 total views, 0 views today